The problem is compounding. AI is being deployed into underwriting, claims, and sales workflows faster than compliance infrastructure can govern it. According to NAIC surveys, 88% of auto insurers and 70% of home insurers currently use or plan to use AI and machine learning models, yet only 7% have successfully scaled these systems enterprise-wide. This creates regulatory exposure that multiplies the original compliance challenge: not only must organizations monitor traditional workflows, but they must now govern AI systems that make or influence decisions across the policy lifecycle.

This guide covers how AI transforms compliance monitoring capabilities, where AI applies across the policy lifecycle, the NAIC regulatory framework and what it demands, and how to implement AI governance that satisfies examiners.

Key Takeaways

- AI enables real-time compliance monitoring across the full policy lifecycle,catching violations before they become regulatory issues

- Adaptive AI systems interpret regulatory language and apply it across multi-state operations without manual IT intervention per rule change

- The NAIC Model Bulletin (Dec 2023) and FACTS principles are adopted in 24+ states,compliance teams should expect active examiner scrutiny now

- Insurers retain full regulatory responsibility for AI systems, whether built in-house or sourced from vendors

- Runtime governance enforces policies at execution, not just configuration, bridging the gap between AI pilots and production compliance

Why Traditional Insurance Compliance Software Falls Short

Rule-based compliance systems operate on explicit if-then logic and break down when encountering novel regulatory scenarios, jurisdictional edge cases, or situations not explicitly programmed. Every regulatory change requires IT resources to update rule sets, creating operational delays that leave gaps in coverage.

When Colorado implements quantitative testing requirements for unfair discrimination while New York mandates comprehensive ECDIS (External Consumer Data and Information Sources) assessments, static rule engines require separate development cycles for each jurisdiction. That process can take weeks or months while compliance exposure quietly accumulates.

The scale problem is equally severe. Compliance spans sales workflows, policy administration, claims handling, and underwriting decisions,each governed by different requirements across 50 state jurisdictions. Manual review processes create inconsistency where compliance outcomes depend on which individual reviewer handles a case rather than on standardized, auditable procedures.

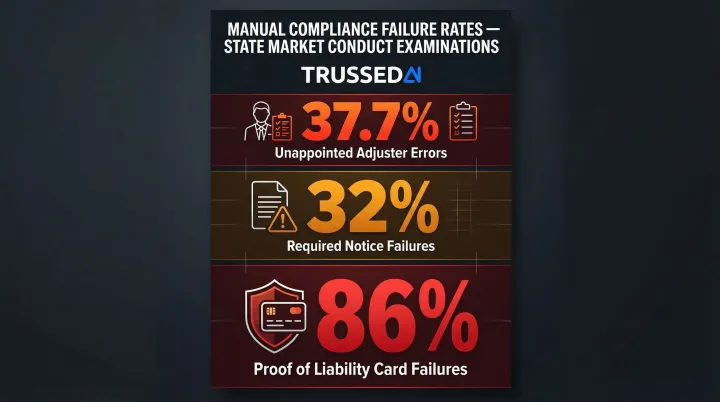

State market conduct examinations consistently expose the failure rate of manual compliance:

- 37.7% error rate for using unappointed adjusters

- 32% failure rate in providing required notices

- 86% failure rate in issuing proof of liability insurance cards

These are systematic failures documented in routine examinations, not edge cases.

The harder problem: insurers are now layering AI into the same workflows where manual compliance is already breaking down. 88% of P&C insurers have implemented AI in some capacity, yet most cannot scale those systems into production. The missing piece isn't the AI itself - it's the runtime controls for real-time policy enforcement, jurisdictional guardrails, and audit-ready evidence generation that regulated deployment actually requires.

How AI Transforms Insurance Compliance Software

From Periodic Audits to Real-Time Continuous Monitoring

Traditional compliance discovers violations after the fact during scheduled audits. AI-powered systems monitor transactions as they happen,moving compliance from reactive remediation to proactive prevention. The operational and financial difference is substantial: catching a claims handling deadline violation before it becomes a regulatory finding versus during an annual examination means avoiding penalties, remediation costs, and reputational damage.

Consider claims deadline compliance. Manual systems rely on periodic reviews that sample a subset of claims weeks or months after decisions were made. AI systems monitor every claim in real time, tracking statutory timeframes and alerting compliance teams before violations occur. When Florida regulators penalized eight insurers $2,075,000 for claims-handling misconduct following hurricanes, the violations included failures to acknowledge claims timely,precisely the type of deadline violation that real-time monitoring prevents.

Real-time monitoring only works when the data is complete. AI enables multi-system data orchestration, pulling from policy administration systems, claims platforms, underwriting databases, and CRM systems to assemble a unified compliance picture that rule-based tools operating in silos cannot achieve.

Key Capabilities AI Adds to Compliance Software

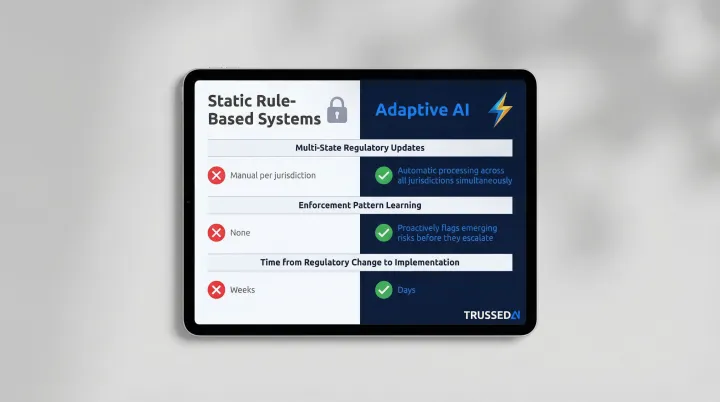

Adaptive Regulatory Interpretation

When 24 states adopted the NAIC Model Bulletin with varying modifications, keeping rule sets current became a maintenance problem for compliance teams. Adaptive AI interprets regulatory language and learns from patterns without requiring a development cycle for every new requirement. These systems process jurisdiction-specific variations and apply them automatically , reducing IT dependency and cutting the lag between regulatory change and operational compliance.

Key advantages over static rule-based systems:

- Processes multi-state regulatory variations without manual rule-set updates per jurisdiction

- Learns from enforcement patterns to flag emerging risk areas before they become violations

- Reduces time from regulatory change to implementation from weeks to days

NLP for Unstructured Compliance Data

Unstructured sources , call notes, claim narratives, agent emails, needs-analysis documentation , contain compliance signals that structured rule engines simply cannot read. NLP closes that gap. A product management study published on ResearchGate found that transformer-based NLP architectures achieve 89% recall in compliance detection compared to 68% for rules-based systems, while reducing manual review rates by 60.5%.

This matters most for sales workflow compliance and needs-analysis documentation, where the evidence is almost entirely free-text and periodic sampling misses too much.

Automatic Audit Trail Generation

Traditional compliance teams spend hundreds of hours reconstructing audit trails when examiners request documentation. AI-powered systems eliminate that burden entirely , governance evidence is generated as a byproduct of every monitored transaction.

Complete records maintained automatically include:

- Policy evaluation results with timestamps

- Data lineage from source systems to compliance decision

- Decision chains showing what triggered each alert or clearance

- Examiner-ready exports requiring no additional preparation

AI Compliance Monitoring Across the Insurance Policy Lifecycle

Sales Workflow Compliance

AI monitors insurance agent qualification requirements in real time,continuously validating license status, territorial authorization, and product line credentials before sales workflows advance. When Massachusetts regulators fined a New York-based agency $2,500 for selling 34 policies while its non-resident license was expired, the violation resulted from a gap in manual license monitoring. AI systems prevent unauthorized sales activities by checking credentials at the point of transaction, not weeks later during periodic reviews.

Beyond licensing, AI enforces needs-analysis documentation standards by validating completeness, accuracy, and regulatory adequacy before transactions proceed. This replaces the manual review step that historically created bottlenecks and inconsistencies across sales teams.

Policy Administration and Claims Handling Compliance

AI automatically applies the correct jurisdiction-specific regulatory requirements to endorsements, renewals, and modifications, flagging gaps before they require manual remediation. Tracking NAIC Model Bulletin adoption across states is not straightforward: some states adopted the bulletin verbatim, while others like Colorado added mandatory quantitative testing requirements. That variation demands dynamic policy application that static rule sets cannot deliver.

Claims deadline tracking is equally high-stakes. AI monitors open claims against state-specific statutory timeframes and alerts compliance teams before violations occur. The litigation risk is concrete: in Estate of Lokken v. UnitedHealth Group, plaintiffs alleged that an insurer used an AI tool to deny claims by supplanting physician decision-making. The federal court granted discovery into how the AI program works and whether it was designed to replace human review. That ruling signals that audit-ready human oversight documentation is now a litigation necessity, not a best practice.

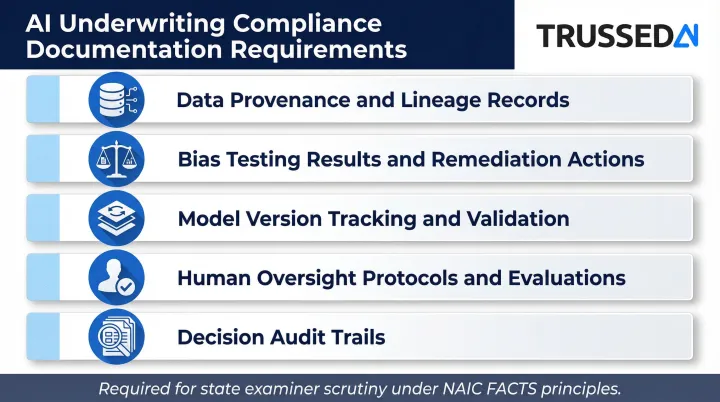

Underwriting Compliance

AI standardizes underwriting procedures by ensuring that AI-assisted risk decisions are documented for fairness and non-discrimination. State regulators are actively developing examination tools to scrutinize how AI models influence underwriting outcomes, making documentation a compliance requirement rather than an internal preference. Compliance teams should maintain:

- Data provenance and lineage records

- Bias testing results and remediation actions

- Model version tracking and validation procedures

- Human oversight protocols and effectiveness evaluations

- Decision audit trails showing who or what made each determination and why

The NAIC Framework and What It Demands of AI Governance

The NAIC Model Bulletin (December 2023) establishes the FACTS principles: Fairness, Accountability, Compliance, Transparency, and Security. While the bulletin is not itself legally binding, 24 states have adopted it as of March 2025, with additional states enacting related regulations. The regulatory trajectory points toward enforceable examinations where state regulators will scrutinize AI governance frameworks with the same rigor they apply to traditional compliance.

State examiners will look for evidence of:

- Documentation of data quality, integrity, and bias analysis for AI-assisted decisions

- Records showing who or what made each determination and why, including validation and testing procedures

- Procedures confirming that human oversight is consistently and meaningfully contributing to decisions , not just nominally present

- Ongoing assessment of AI system reliability and output quality to catch model drift

The NAIC's position on third-party AI accountability is explicit: insurers retain full regulatory responsibility for the AI systems they deploy, regardless of whether those systems are built internally or sourced from vendors. The bulletin states that an insurer's AI Systems Program "should address the AI Systems used with respect to regulated insurance practices whether developed by the Insurer or a third-party vendor."

That accountability extends into vendor contracts. Insurers must maintain due diligence records, contractual safeguards, and governance documentation for every vendor-supplied AI system , the same documentation regulators will request during an examination.

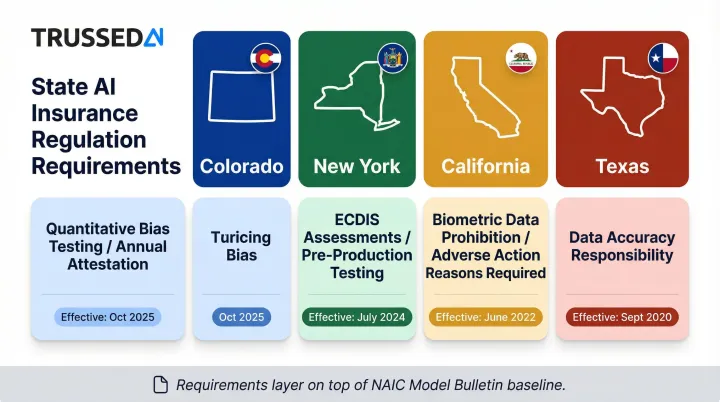

That vendor accountability burden multiplies across jurisdictions. Each state layering its own AI requirements on top of the NAIC baseline forces insurers to track compliance against a moving, multi-jurisdiction target:

| State | Key Requirements | Effective Date |

|---|---|---|

| Colorado | Quantitative testing to detect and remediate unfair discrimination with respect to race; annual attestation filing | Oct 15, 2025 |

| New York | Comprehensive assessments proving ECDIS/AI guidelines don't unlawfully discriminate; testing prior to production and on regular cadence | July 11, 2024 |

| California | Prohibition on biometric data for claims; specific reasons required for adverse actions using complex algorithms | June 30, 2022 |

| Texas | Strict responsibility for data accuracy in rating, underwriting, and claims handling, even if provided by third parties | Sept 30, 2020 |

Static compliance configurations , rules set once and applied uniformly , cannot handle this kind of divergence. A governance layer that enforces jurisdiction-specific policy rules at runtime, per interaction, is the practical minimum for operating across these states.

Building an AI Governance Layer for Insurance Compliance

Deploying AI to do compliance work is fundamentally different from governing the AI that does compliance work. Most insurance organizations can demonstrate AI compliance capabilities in pilots but struggle to enforce consistent governance at runtime across all models, agents, and workflows in production. The data confirms this: while 88% of organizations report regular AI use, only 7% have successfully scaled AI systems enterprise-wide.

That scaling gap is largely a governance gap. A runtime governance control plane enforces compliance policies at the moment AI models make decisions , not just at configuration time. Rather than relying on static policy documentation, it applies active control that evaluates policies before every AI interaction executes.

Trussed AI's platform acts as a drop-in proxy that enforces policies in real time across AI apps, agents, and developer tools with zero changes to application code. It sits directly in the flow of AI interactions, intercepting requests at the API level and applying configured policies transparently.

For insurance workflows, this means every claims automation request, underwriting assistance query, or fraud detection analysis passes through governance enforcement before execution. Audit-ready compliance evidence is generated as a byproduct of every governed interaction.

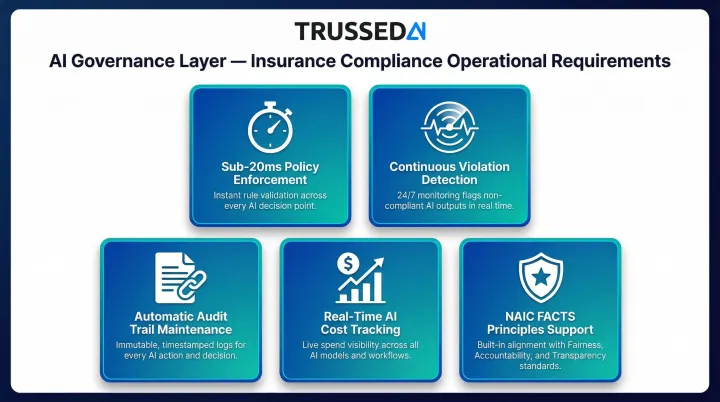

The operational requirements such a governance layer must meet for insurance use include:

- Enforces policies in under 20ms to avoid disrupting customer-facing workflows

- Monitors compliance continuously, with violation detection rates exceeding manual review

- Maintains complete audit trails automatically , capturing policy evaluation results, model versions, timestamps, and data lineage

- Tracks AI costs in real time across teams, models, and applications for financial accountability

- Supports NAIC FACTS principles through fairness testing, accountability documentation, transparency controls, and security enforcement

Trussed AI's enterprise security posture provides additional assurance relevant for regulated industry deployments, demonstrating that the governance platform itself meets enterprise security and compliance standards.

How to Implement AI in Insurance Compliance Software

Begin with a single compliance subdomain rather than attempting broad simultaneous deployment. Start with regulatory reporting, claims deadline monitoring, or sales documentation validation,whichever represents the highest compliance risk or consumes the most manual review time. Success in one subdomain creates a replicable template for expanding AI governance across the full compliance function.

Establish success metrics before deployment:

- Compliance review cycle time reduction

- Detection accuracy rates compared to manual baseline

- False positive rates that create unnecessary review burden

- Reduction in audit preparation hours

Data infrastructure is a prerequisite. AI compliance systems require unified, reliable data across policy administration, claims, underwriting, and regulatory systems. Fragmented data foundations are the primary reason AI compliance pilots fail to scale.

Gartner predicts that through 2026, organizations will abandon 60% of AI projects unsupported by AI-ready data. Audit and unify your data sources before deploying AI monitoring , gaps in coverage undermine the entire governance layer.

Frame AI to compliance teams as executing your documented procedures, not replacing human judgment. When reviewers understand that AI enforces the best practices your team already defined, adoption follows naturally , and that internal confidence is what carries pilots into production.

Frequently Asked Questions

How is AI used in compliance monitoring?

AI monitors transactions in real time against regulatory requirements, flagging potential violations before they surface in periodic audits. It pulls data simultaneously from policy administration, claims, underwriting, and CRM systems to build a unified compliance picture across the organization.

Can AI do compliance work?

AI executes documented compliance procedures consistently across every transaction, but does not replace compliance judgment. Rather, it enforces your best practices at scale and surfaces exceptions for human review, maintaining the human oversight that regulators expect.

What ensures compliance with insurance regulations?

Compliance requires documented governance frameworks, real-time monitoring, audit-ready evidence, and adherence to the NAIC FACTS principles (Fairness, Accountability, Compliance, Transparency, and Security). Organizations must demonstrate not just the policies they've established, but that those policies are actively enforced at runtime.

What AI do insurance companies use?

Insurance companies deploy AI across fraud detection, risk scoring, underwriting automation, claims processing, and sales workflow monitoring. Governance platforms are increasingly layered across these systems to enforce policies at runtime and maintain consistent oversight regardless of which models or vendors are involved.

How is AI affecting the insurance industry?

AI is improving operational efficiency across underwriting, claims, and customer service, but it's also creating new governance and regulatory challenges. Capturing those efficiency gains requires structured oversight frameworks that keep pace with evolving regulatory requirements.

Can AI do insurance verification?

AI automates insurance verification tasks, including license validation, coverage confirmation, and document completeness checks, by integrating with policy administration and credentialing systems in real time. This prevents unauthorized sales and policy issuance errors that would otherwise require costly remediation.